As of the first quarter of 2019, more than 50 percent of investment-grade bonds in the United States and globally by amount outstanding are rated Baa, according to Moodys. This is dramatically higher than the lead up to the 2008-09 financial crisis. The total amount outstanding currently hovers around $5 trillion.

The concern levied by the rating agencies, as well as Fed mucky mucks, is a fallen-angel scenario whereby a downgrade from Baa leads to a high-yield or junk-bond status and a big air pocket in prices. Most institutions and pension funds are required to hold only so-called “investment grade” notes. BAA is the lowest “investment grade” rating.

The portion of the Ponzi scheme pyramid that implodes first are the lower-grade bonds. During the last two years, downgrades in the B- and below markets have increased steadily. This is probably the reason the Fed has started “Not QE 4.” Will it work? We doubt it, as the emperor wears no clothes.

An industry in which a bond bust is well underway is the extremely capital intensive energy fracking sector. Chesapeake Energy’s (CHK) debt is nearly $10 billion. In a Nov. 5 SEC filing, the company warned of its own demise unless oil and gas prices surge sky high ASAP:

“If continued depressed prices persist, combined with the scheduled reductions in the leverage ratio covenant, our ability to comply with the leverage ratio covenant during the next 12 months will be adversely affected which raises substantial doubt about our ability to continue as a going concern.”

Even as late as mid-year, 2019, CHK’s senior unsecured debt was trading near-par. The slide is pronounced, and now Wall Street is abandoning the company with a round of sells and downgrades. This demonstrates how suddenly a bond bust can manifest itself.

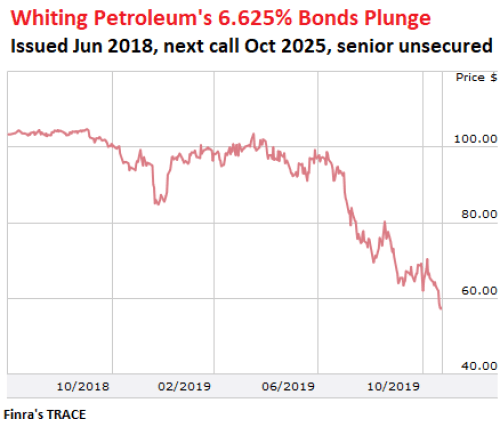

Another big name in fracking debt is Whiting, and the chart looks similar.

Domestic oil and gas is a huge business, with lots of high-paying jobs, not only in the oil field but in technology sectors, including software and hardware, manufacturing of heavy equipment, transportation, materials and, of course, construction.

As oil-field rig counts drop, there go good jobs in an important sector.

Wolf Street has these comments on the “tech” and unicorn market.

He states: “There is a slew of big publicly traded companies that stopped being startups years ago, that are burning huge amounts of cash to this day and that need to constantly get even more cash from investors to have more fuel to burn. This includes Tesla, which succeeded in extracting another $2.7 billion in cash in early May from investors. Tesla duly rushed to burn this cash. And it also includes Netflix, which extracted another $2.2 billion in April. From day one, these two companies – just Netflix and Tesla alone – have burned tens of billions of dollars in cash and continue to do so, though they’re mature companies.

This also includes Uber, which received another $8 billion from investors during its IPO in May. It’s now busy burning up in its furnace.

Then there is the WeWork Ponzi. WeWork’s $702 million unsecured 7.875% bonds, issued in April last year and due in May 2025 – its only publicly traded securities – dropped to 74.44 cents on the dollar, down 29% from $1.05 in mid-August before the death spiral began.

Read “Is SoftBank’s Bailout of WeWork Already in Trouble?”

Will “punters” start seeing these schemes for what they really are, Ponzi units? Will they suddenly become reluctant to get cleaned out, refuse a bail out and remunerate existing investors? Will suddenly the money run out?

So far, despite this crack, there is no employment crisis. We haven’t seen millions of people getting laid off — yet.

Meanwhile, throughout the last several years, subprime lenders have charged blistering, usurious interest rates to debtors with poor incomes and little ability to service the loan.

The delinquency rate on credit card loan balances at the nearly 5,000 smaller commercial banks in the U.S. is blowing out, according to Federal Reserve data. This means all banks except the largest 100. During the third quarter, the delinquency rate at these banks rose to 6.25%. That’s higher even than during the peak of the financial crisis.

Back in 2016, the credit card delinquency rate at these banks was in the 3% range. It has more than doubled in two years.

One group of credit card consumers isn’t calculated in interest-bearing credit card debt. It’s those who use their credit cards only as payment system and to get perks but pay off their cards every month, carry no balances and pay no interest or fees.

On the other side are consumers with maxed-out credit cards or with large balances, and they have personal loans, payday loans, etc. They’re sitting ducks for the lending industry, because they cannot pay off the loans but pay interest and fees out of their nose, wobble from paycheck to paycheck and, if something goes wrong, become delinquent. It’s these people who owe the lion’s share of that $1.04 trillion in revolving credit.

In a new study, life insurer and financial services provider Northwestern Mutual found that 45% of Americans that have debt spend “up to half of their monthly income on debt repayment.”

The Federal Reserve found that 46% of adults could not cover an emergency expense of $400, such as a broken windshield.

Subprime auto loans have also been blowing out. In the third quarter, the rate of serious delinquency of the $1.3 trillion in auto loans has risen to 4.71%. In the third quarter, about 21% of all subprime auto loans were seriously delinquent, meaning 90 days past due.

Incidentally, 4.71% is just above the level of Q3 2009 — months after G.M., Chrysler and Lehman filed for bankruptcy, and when the U.S. was confronting an unemployment crisis. People were defaulting on their auto loans because they had lost their jobs.

The whole auto recovery was pinned entirely on new debt issuance and to more and more marginal debtors.

Lengthening average duration of auto loans was key, with 84 months common and 96 months (8 years) being available. This creates more underwater loans when vehicles are repossessed.

Over the past 10 years, since Q3 2009, auto loan balances have surged 62% compared to population growth of 8%.

Pressuring the lower-credit consumers are the prices of goods and services that they need. Prices have risen sharply, far outpacing incomes. This includes healthcare costs, food, apartment rentals and cars.

Total non-housing consumer debt has skyrocketed in the last decade.

Student loans have soared in the last decade despite declining college enrollment. According to the latest data from the National Center for Education Statistics, enrollment fell by 7% between 2010 and 2017. But those fewer and fewer students are borrowing more and more to pay for tuition, transportation, rent, electronic devices and other things on which the corporate university financial complex gets rich.

Wolf Street adds: “A whole sub-economy has sprung up to leech this money out of the educational process and taxpayers via student loans. Students are the money conduit from the taxpayer to:

- Universities trying to grow their empires

- Corporations, such as Apple, selling their products to students

- Textbook publishers with monopolistic rip-off strategies

- Landlords seeking a high yields on their investment, and Wall Street seeking fees on securitizing real estate debt

- Ticket vendors, grocery stores, bars, restaurants, car dealers, airlines and others

“Student housing” has become a hugely hyped asset class with its own student-housing Commercial Mortgage Backed Securities in which delinquency rates are now spiking.

National debt has increased $1.3 trillion in the last 12 months under faux-“conservative” Trump and his Democrat co-conspirators.

Self-Destructive Consumerism and Materialism as Mental Illness

Hyper-consumerism is a form of collective, psychotic mental illness. It leads to narcissistic behaviors and poor self-control. The idea of spending money you don’t have on some hyped up good or gadget apparently is an endorphin that relieves depression — at least momentarily.

Human beings are an incredibly social species, one of the few that spend their entire lives in groups. The trick is to convey a sense of belonging to other zombies who have the same need to be constantly consuming and in turn, burying themselves financially. I picture it as a circle jerk.

This type of mental illness is a social and cultural problem that stems from 24/7 media brainwashing of a Luciferian nature. Although twisted and warped pharma tries to exploit this mental condition with drugs, no drug can counter this. Such behavior is also obedience to authority and the usurers.

I would suggest that the depression itself may be your psyche’s natural way of rejecting or countering mind control and maintaining a sense of reality and truth. Does the depression come from the narcissism and lack of moral clarity (aka Luciferian moral relativism)?

The best deprogramming is to turn off most mind-numbing entertainment and media, or at least wean off that narcotic as much as possible. That is also an act of true defiance against the exploiters and manipulators. Otherwise you are merely talkin’ the talk.

And being labelled “maladjusted” to this reigning dominant form of low culture may very well be a sign of a healthy human being.

Finally, the emergence and sick promotion of the genderless society and sexual confusion is bound to make many people mentally ill and depressed. This is in direct confrontation with hundreds of generations of inherited nature and DNA.

I suspect that the US government is reprising the strategy from the 1980s of forcing down oil/natgas prices no matter what in order to deprive Russia of export earnings. This explains why the federal government doesn’t really restrict fracking despite their climate change hysteria. The money poured into the system by the fed also helps.

Oh, it’s going to be a long winter. Dammit, now I need a prescription for anti-depressants.

I am absolutely joyous reading your work. I am 63……I have known these things since I was 23. I used to feel utterly alone seeing the blatant luciferian reality. With the internet I realized I was not alone and when I see the work on this website in particular I know absolutely that no matter how small the numbers may be, we have the Victory.

The ‘national debt’ is an interesting animal…despite ridiculous claims that the ‘biggest owner of the debt is you’ it would appear that in essence dollars are created by the federal reserve banks and the global oligarchs behind them and lent at interest to US tax payers.

https://www.thebalance.com/who-owns-the-u-s-national-debt-3306124

The interest on this magic money has accumulated for decades with predictable unsustainable results….

Dear Diane,

Our numbers aren’t as small as you might think… Although the numbers are inconsequential when you take into account that the ALMIGHTY is on our side. They’ve always lost, they were born and made to lose- they’re just in the process of figuring that out, the prideful wretches that they are. They could control their own destiny (read survival) if they’d show an ounce of humility, and so they seal their own fate in their refusal to repent from their lecherous ways. Let them burn-the lack of grace they have shown upon others will shine upon them and theirs in the precise proportion in which they have inflated the medium of exchange over the past 1500 years. There’s an awful storm coming, and we’re just waiting for these soft bodied/handed intelligence faggots to set it off. JUST. WAITING. As a once very wise ww2 Japanese general said referring to the the hypothetical land takeover of the USA- “it’s impossible- there’d be a rifle behind every blade of grass”- this is still the reason that holds these soft handed bitches back. Hence, plan b-pro-miscegenation-debt-BIG$cultural warfare-SLOW KILL…Ain’t gonna happen. Unfortunately for them, we can’t die fast enough… GRACE manifests itself as needed, AD INFINITUM. Eph 6:12

Dear Darryl

I Thank for your response – I do know that one with Yahweh is an army. I know the weapon I am to use for it is the sword of Yahweh which is the Word of Yahweh and I am well versed in the Word of Yahweh. I look forward to the battle and I look forward to seeing the destruction of the enemy. I know absolutely that my enemies are the offspring of Cain – the vagabond imposters. I include all those that have supported the imposter vagabonds knowing absolutely what they are. Unfortunately the apathetic are the biggest disgrace in this country….sheep led to slaughter willingly by the judas goats and there are many. I see the Trump card being played and the sheep willingly falling into a trance. I have seen many things in my life and the luciferian agenda was blatantly obvious to me in my youth and it is blatantly obvious to me now. I know now that there are many on the watchtower that are watching and warning…..it is easy to discern those that are not but pretend to be watchmen. No one can leave the Almighty out of this battle for to do so is to fail. We with Yahweh will not fail that is His promise and not mine. For we are David and we are Gideon and we will have the Victory as it is written in Deuteronomy 32……He is our Rock and He will fight with us and for us. I hope to see you in the battle soon. May Yahweh bless and guide you always.

Thanks for this. It is just more proof that what Gail Tverberg speaks on over at the ourfiniteworld blog about our problems in the oil and gas sector is low prices. This is what will eventually crash and burn the entire system. We have a serious affordability problem right across the board.