In my recent podcast with Robert Phoenix- Robert Phoenix and Russ Winter Discuss the Neoliberal Political Grift Economy – I laid out the economic forecast that a replay or template of the 1907 Panic is unfolding. Go to 1:39:00 for the explanation.

Effectively the mega companies somehow brilliantly timed (skill, luck or tipped off?) the Fed rate increases and insolated themselves. Smaller and medium sized companies are more tied to credit lines and lower rated corporate or junk bond borrowings. Thus interest cover is far lower than the big boyz. And this chart is using 2022 financials. The situation is much worse now.

Readers can also refer to my post George Cortelyou, President McKinley’s Assassination and the Panic of 1907 to understand this. Effectively JP Morgan consolidated the US regional and small bank sector during the Panic. This Panic will consolidate under mega multi-nationals.

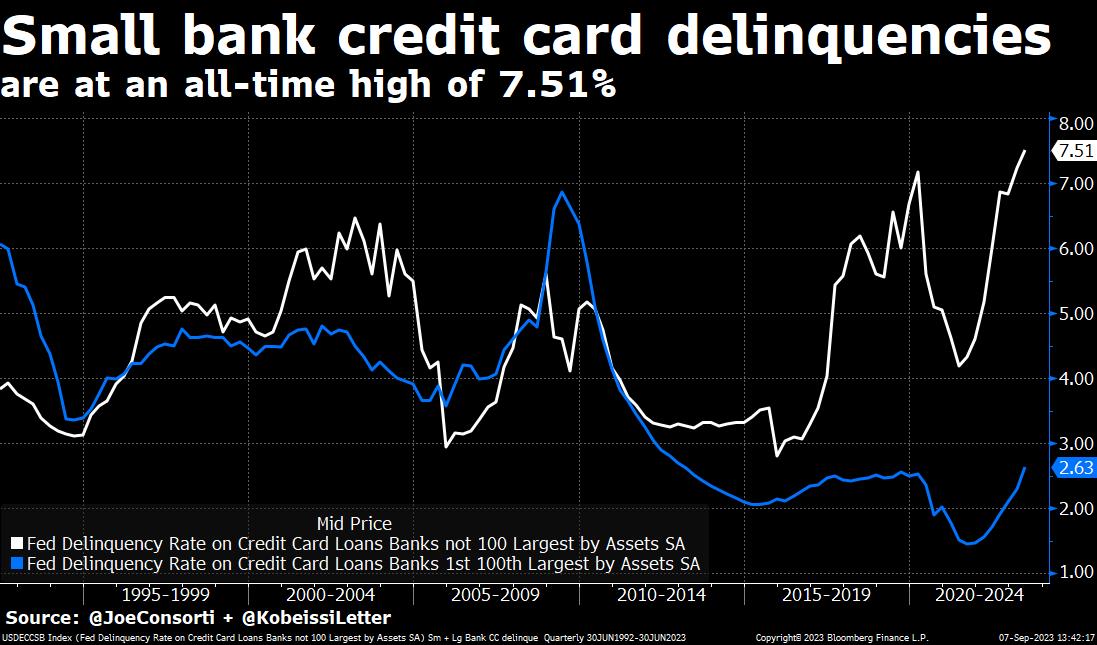

Now we see the advantages the larger banks have with their prime credit card markets. The smaller banks lend to the ever growing have nots in American society. The have nots have larded up on expensive usurious debt. With student loans needing to be repaid, and excess savings from the scamdemic largesse depleted, a large delinquency gap is opening up and climbing. There are 45 million people in the US with student debt totaling $1.6 trillion.

Countdown to Economic Oblivion

Average family receiving food stamps saw loss of $250/month

Americans have already started repaying their student loans en masse

Treasury data shows more than $6.4B was paid to the Department of Education in August—which would imply a ~$65B annual cut to household incomes compared to April, and payments are likely to increase from here pic.twitter.com/O8hOhHCckI

— Joey Politano 🏳️🌈 (@JosephPolitano) September 1, 2023

In a perfect storm, and as draining the now depleted Strategic Petroleum Reserve has ended, energy prices are surging again.

Note that prime lenders – in blue – have barely budged. Notice however that in 2008-2009 during that financial crisis and bubble bursting, the blue line spiked. With wallets empty for the have nots the white line is going parabolic.

The trouble for most consumers is flashing red. On September 7 a large player in the used car market went under.

Major player in used cars just got wiped out 🤯

the internal memo below:

“Elevated pricing and rising interest rates have further deteriorated conditions in the automotive retail market, weakening consumer demand and affordability.” pic.twitter.com/aBbvre9fjC

— CarDealershipGuy (@GuyDealership) September 6, 2023

Auto lenders are closing shop.

Another blow to auto lending:

CIG Financial is out.

Will only serve AutoNation stores moving forward. pic.twitter.com/IvMMSYmAxd

— CarDealershipGuy (@GuyDealership) September 1, 2023

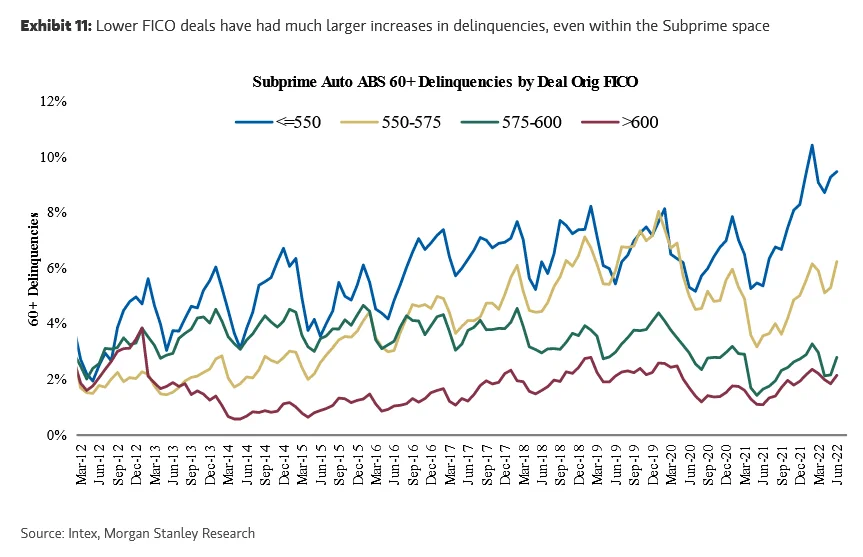

Subprime auto delinquencies were edging higher even before the exhaustion of excess savings and the renewal of student loan repayments. Haves hanging in there, they will need a market bust and credit crisis/panic.

Additionally smaller and mid-size banks, hold 71% of commercial real estate loans (CRE). The word is that many of these loans are already in extend and pretend mode.

Demand for CRE loans is now at its lowest since 2008. This comes as the price of office buildings is down 30% in one year. Office vacancy rates just hit a record 13.1%, up 6 straight quarters, and adding more pressure on CRE. Woke policies have ruined cities like San Francisco, see San Francisco’s Woke Bust.

Meanwhile, there is nearly $1.5 trillion in CRE debt that needs to be refinanced by 2025. Rates on these loans are set to more than double since they were last financed.

Additionally, small and mid-size banks larded up on investment securities such as 3% mortgages during the Fed’s great low interest mistake during the scamdemic.

These are now marked at substantial losses. Several of the worst offenders failed last spring, but there are more walking dead remaining.

Another problem for the smaller banks lies in a bank walk as deposits seek higher return in the treasury bills or money markets. The dire condition of these banks haven’t even factored in- yet. When the realization hits, the bank panic a la 1907 will ensue.

thanks for the time stamp on the podcast. enjoyed you and Bob’s insight.